Question No 47 Chapter No 13

Additional Question

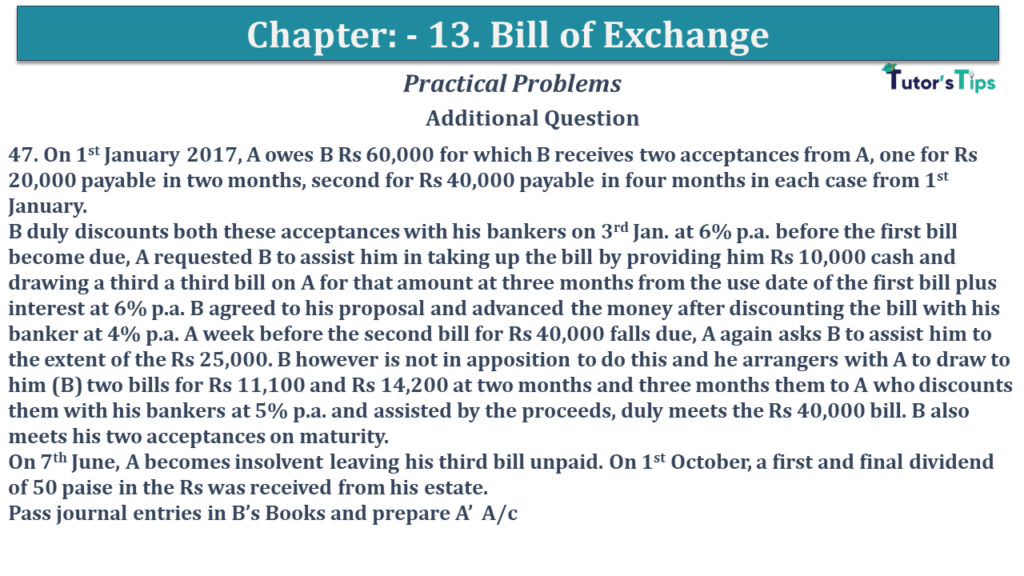

47. On 1st January 2017, A owes B Rs 60,000 for which B receives two acceptances from A, one for Rs 20,000 payable in two months, second for Rs 40,000 payable in four months in each case from 1st January.

B duly discounts both these acceptances with his bankers on 3rd Jan. at 6% p.a. before the first bill become due, A requested B to assist him in taking up the bill by providing him Rs 10,000 cash and drawing a third a third bill on A for that amount at three months from the use date of the first bill plus interest at 6% p.a. B agreed to his proposal and advanced the money after discounting the bill with his banker at 4% p.a. A week before the second bill for Rs 40,000 falls due, A again asks B to assist him to the extent of the Rs 25,000. B however is not in apposition to do this and he arrangers with A to draw to him (B) two bills for Rs 11,100 and Rs 14,200 at two months and three months them to A who discounts them with his bankers at 5% p.a. and assisted by the proceeds, duly meets the Rs 40,000 bill. B also meets his two acceptances on maturity.

On 7th June, A becomes insolvent leaving his third bill unpaid. On 1st October, a first and final dividend of 50 paise in the Rs was received from his estate.

Pass journal entries in B’s Books and prepare A’ A/c

The solution of Question No 47 Chapter No 13: –

| In the books of …. |

|||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2017 | |||||

| Jan.1 | Bill Receivable A/c(i) | Dr. | 20,000 | ||

| Bill Receivable A/c(ii) | Dr. | 40,000 | |||

| To A A/c | 60,000 | ||||

| (Being Acceptance received ) | |||||

| Jan.3 | Bank A/c | Dr. | 59,000 | ||

| Discount Charges A/c | Dr. | 1,000 | |||

| Bill Receivable A/c | 60,000 | ||||

| (Being three bill drawn on Y ) | |||||

| Mar.4 | A A/c | Dr. | 150 | ||

| To Interest A/c | 150 | ||||

| (Being interest debited to A) | |||||

| Mar.4 | Bill Receivable A/c(iii) | Dr. | 10,150 | ||

| To A A/c | 10,150 | ||||

| (Being acceptance received) | |||||

| Mar.4 | Bank A/c | Dr. | 10,048 | ||

| Discounting charges A/c | Dr. | 102 | |||

| To Interest A/c | 10,150 | ||||

| (Being interest charged on Arjun) | |||||

| Mar.4 | A A/c | Dr. | 10,000 | ||

| To Bank A/c | 10,000 | ||||

| (Being cash paid to A) | |||||

| May.4 | A A/c | Dr. | 25,300 | ||

| To Bill payable A/c(i) | 11,100 | ||||

| To Bill payable A/c(ii) | 14,200 | ||||

| (Being bill endorsed to Y) | |||||

| Jun.4 | A A/c | Dr. | 10,150 | ||

| To Bank A/c | 10,150 | ||||

| (Being third bill dishonoured) | |||||

| Jul.7 | Bill payable A/c(i) | Dr. | 11,100 | ||

| To Bank A/c | 11,100 | ||||

| (Being first acceptance paid) | |||||

| Aug.4 | Bill payable A/c(ii) | Dr. | 14,200 | ||

| To Bank A/c | 14,200 | ||||

| (Being second acceptance paid) | |||||

| Aug.4 | Bank A/c | Dr. | 17,725 | ||

| Bad debts A/c | Dr. | 17,725 | |||

| To A A/c | 35,450 | ||||

| (Being 50 paise per Rs received in full settlement ) | |||||

| Dr. | A A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 2018 | 2018 | ||||||

| Jan.1 | To Balance b/d | 60,000 | Jan.1 | By Bill Receivable A/c(i) | 20,000 | ||

| Mar.4 | To Interest A/c | 150 | Jan.1 | By Bill Receivable A/c(ii) | 40,000 | ||

| Mar.4 | To Bank A/c | 10,000 | Mar.4 | By Bill Receivable A/c(iii) | 10,150 | ||

| Mar.4 | To Bill Payable A/c(i) | 11,100 | |||||

| Mar.4 | To Bill Payable A/c(ii) | 14,200 | |||||

| Jun.7 | To Bank A/c | 10,150 | |||||

| May. 31 | By Balance c/d | 34,450 | |||||

| 1,05,600 | 1,05,600 | ||||||

https://tutorstips.com/bills-payable/

Also, Check out the solved question of all Chapters: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.

Advertisement