Question No 37 Chapter No 5

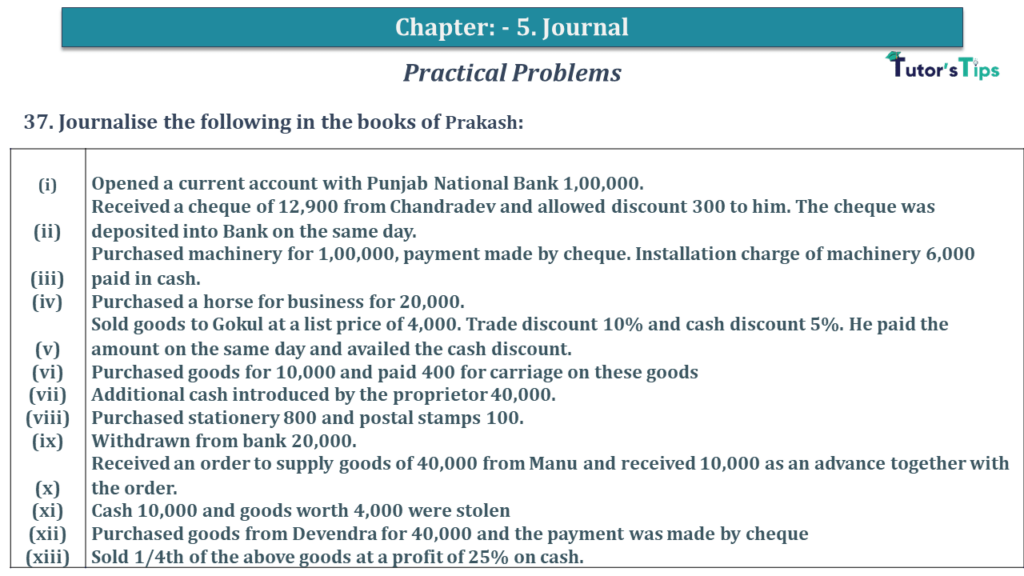

37. Journalise the following in the books of Prakash:

| (i) | Opened a current account with Punjab National Bank 1,00,000. |

| (ii) | Received a cheque of 12,900 from Chandradev and allowed discount 300 to him. The cheque was deposited into Bank on the same day. |

| (iii) | Purchased machinery for 1,00,000, payment made by cheque. Installation charge of machinery 6,000 paid in cash. |

| (iv) | Purchased a horse for business for 20,000. |

| (v) | Sold goods to Gokul at a list price of 4,000. Trade discount 10% and cash discount 5%. He paid the amount on the same day and availed the cash discount. |

| (vi) | Purchased goods for 10,000 and paid 400 for carriage on these goods |

| (vii) | Additional cash introduced by the proprietor 40,000. |

| (viii) | Purchased stationery 800 and postal stamps 100. |

| (ix) | Withdrawn from bank 20,000. |

| (x) | Received an order to supply goods of 40,000 from Manu and received 10,000 as an advance together with the order. |

| (xi) | Cash 10,000 and goods worth 4,000 were stolen |

| (xii) | Purchased goods from Devendra for 40,000 and the payment was made by cheque |

| (xiii) | Sold 1/4th of the above goods at a profit of 25% on cash. |

The solution of Question No 37 Chapter No 5: –

| In the Books of Radhika Traders |

|||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2019 | |||||

| i | Bank A/c | Dr. | 1,00,000 | ||

| To Cash A/c | 1,00,000 | ||||

| (Being opened a bank account in PNB) | |||||

| ii | Bank A/c | Dr. | 12,900 | ||

| Discount Allowed A/c | Dr. | 300 | |||

| To Chandra dev | 13,200 | ||||

| (Being received cheque from Chandradev and allowed discount) | |||||

| iii | Machinery A/c | Dr. | 1,06,000 | ||

| To Bank A/c | 1,00,000 | ||||

| To Cash A/c | 6,000 | ||||

| (Being machinery purchased and installation charges paid) | |||||

| iv | Livestock A/c | Dr. | 20,000 | ||

| To Cash A/c | 20,000 | ||||

| (Being purchased horse for business) | |||||

| v | Cash A/c | Dr. | 3,420 | ||

| Discount Allowed A/c | Dr. | 180 | |||

| To Machinery A/c | 3,600 | ||||

| (Being sold goods to Gokul and received payment) | |||||

| vi | Purchases A/c | Dr. | 10,000 | ||

| Carriage inwards A/c | Dr. | 400 | |||

| To Cash A/c | 10,400 | ||||

| (Being purchases made and carriage paid) | |||||

| vii | Cash A/c | Dr. | 40,000 | ||

| To Capital A/c | 40,000 | ||||

| (Being capital introduced) | |||||

| viii | Stationery A/c | Dr. | 800 | ||

| Postage A/c | Dr. | 100 | |||

| To Cash A/c | 900 | ||||

| (Being stationery & postal stamps bought) | |||||

| ix | Cash A/c | Dr. | 20,000 | ||

| To Bank A/c | 20,000 | ||||

| (Being with drawn from bank) | |||||

| x | Cash A/c | Dr. | 10,000 | ||

| To Manu Advance A/c | 10,000 | ||||

| (Being Advance received from Manu) | |||||

| xi | Loss by theft A/c | Dr. | 14,000 | ||

| To Purchases A/c | 4,000 | ||||

| To Cash A/c | 10,000 | ||||

| (Being cash & goods stolen) | |||||

| xii | Purchases A/c | Dr. | 40,000 | ||

| To Bank A/c | 40,000 | ||||

| (Being goods purchased payment made by cheque) | |||||

| xiii | Cash A/c | Dr. | 12,500 | ||

| To Sale A/c | 12,500 | ||||

| (Being goods sold at the profit of 25%) | |||||

Working Note: –

Calculation of payment made and outstanding amount to Arun*

| Cost | = | 2,00,000 |

| Less: Trade discount on (15% on 66,000) | = | 30,000 |

| = | 1,70,000 | |

| Payment made in cash | = | 1,36,000 |

| Less: cash discount (2% on 1,36,000 | = | 2,720 |

| = | 1,33,280 |

Advertisement

https://tutorstips.com/journal-entries/

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

Chapter 1 Evolution of Accounting & Basic Accounting Terms

Advertisement

Chapter 2 Accounting Equations

Chapter 3 Meaning and Objectives of Accounting

Chapter 5 Books of Original Entry – Journal

Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

Chapter 7 Books of Original Entry – Cash Book (Coming soon)

Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

Advertisement

Chapter 9 Ledger (Coming soon)

Chapter 10 Trial Balance and Errors (Coming soon)

Chapter 11 Bank Reconciliation Statement (Coming soon)

Chapter 12 Depreciation (Coming soon)

Chapter 13 Bills of Exchange (Coming soon)

Advertisement

Chapter 14 Generally Accepted Accounting Principles(GAAP)

Chapter 15 Bases of Accounting

Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

Advertisement

Chapter 17 Capital and Revenue

Chapter 18 Provisions and Reserves

Chapter 19 Final Accounts (Coming soon)

Chapter 20 Final Accounts – With Adjustments (Coming soon)

Chapter 21 Errors and their Rectification (Coming soon)

Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

Chapter 24 Computerised Accounting System (Coming soon)

Chapter 25 Introduction to Accounting Information System (Coming soon)