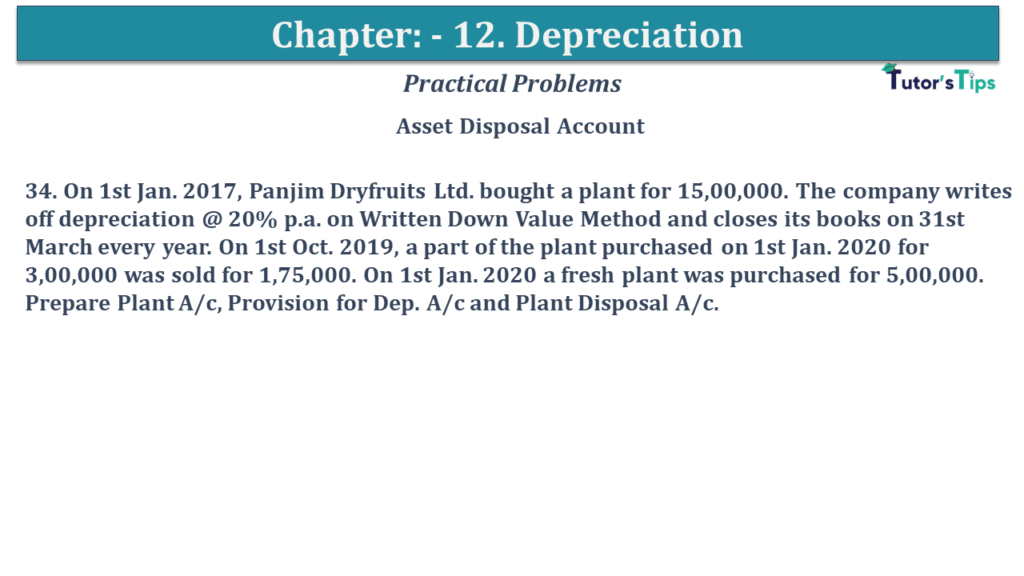

Question No 34 Chapter No 12

34. On 1st Jan. 2017, Panjim Dryfruits Ltd. bought a plant for 15,00,000. The company writes off depreciation @ 20% p.a. on Written Down Value Method and closes its books on 31st March every year. On 1st Oct. 2019, a part of the plant purchased on 1st Jan. 2020 for 3,00,000 was sold for 1,75,000. On 1st Jan. 2020 a fresh plant was purchased for 5,00,000. Prepare Plant A/c, Provision for Dep. A/c and Plant Disposal A/c.

The solution of Question No 34 Chapter No 12: –

| Dr. | Plant A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 1st Jan.2017 | To Bank A/c (3,00,000 + 12,00,000) | 15,00,000 | |||||

| 31st Mar 2017 | By Balance C/d | 15,00,000 | |||||

| 15,00,000 | 15,00,000 | ||||||

| 1st Apr.2017 | To Balance b/f | 15,00,000 | |||||

| 31st Mar 2018 | By Balance C/d | 15,00,000 |

|||||

| 15,00,000 |

15,00,000 |

||||||

| 1st Apr.2018 | To Balance b/f | 15,00,000 | |||||

| 31st Mar 2019 |

By Balance C/d |

15,00,000 | |||||

| 15,00,000 | 15,00,000 | ||||||

| 1st Apr.2019 | To Balance b/f | 15,00,000 | 31st Oct 2019 | By Plant Disposal A/c | 3,00,000 | ||

| 1st Jan.2020 | To Bank A/c | 5,00,000 | |||||

| 31st Mar 2020 |

By Balance C/d |

17,00,000 |

|||||

| 20,00,000 |

20,00,000 | ||||||

| Dr. | Plant Disposal A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 1st Oct 2019 | To Plant A/c | 3,00,000 | 1st Oct 2020 | By Provision for Depreciation A/c | 1,35,840 | ||

| 1st Oct 2020 | To Profit & Loss A/c | 10,840 | 1st Oct 2020 | By Bank A/c (Sale) | 1,75,000 | ||

| 3,10,840 | 3,10,840 | ||||||

| Dr. | Provision for Depreciation A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 31st Mar 2018 | By Depreciation A/c (15,000 + 60,000) | 75,000 | |||||

| 31stMar.2018 | Balance c/d | 75,000 | |||||

| 75,000 | 75,000 | ||||||

| 31st Apr 2018 | By Balance b/d | 75,000 | |||||

| 31st Mar.2018 | Balance c/d | 3,60,000 | 31st Mar 2018 | By Depreciation A/c (57,000 + 2,28,000) | 2,85,000 | ||

| 3,60,000 | 3,60,000 | ||||||

| 31st Apr 2018 | By Balance b/d | 3,60,000 | |||||

| 31stMar.2019 | Balance c/d | 5,88,000 |

31st Mar 2019 |

By Depreciation A/c (45,600 + 1,8,2,400) |

2,28,000 |

||

| 5,88,000 |

5,88,000 |

||||||

| 31stOct.2019 | To Machine Disposal A/c | 1,35,840 | 31st Apr 2019 | By Balance b/d | 5,88,000 | ||

| 1st Oct 2019 | By Depreciation A/c (6 Months) | 18,240 | |||||

| 31stMar.2020 | To Balance b/f | 6,41,230 |

31st Mar.2019 | By Depreciation A/c (1,45,920 + 25,000) | 1,70,920 | ||

| 7,77,160 | 7,77,160 | ||||||

Working Note:

Calculation of Profit or Loss on Sale M1

| Statement Showing the Profit and loss on the sale of Plant | |

| Particulars |

Amount |

| Machinery Purchase on of Equipment as on 1st Jun. 2017 | 3,00,000 |

| Less: – Amount of Depreciation charged on the year 2017-18 | |

| 3,00,000 *20%* 3/12 | 15,000 |

| Amount of Depreciation charged on the year 2017-18 | |

| 2,85,000 *20%* 12/12 | 57,000 |

| Amount of Depreciation charged on the year 2018-19 | |

| 2,28,000 *20%* 12/12 | 45,600 |

| Amount of Depreciation charged on the year 2019-20 | |

| 1,82,400 *20%* 3/12 | 18,240 |

| Book value of asset as of 1st Oct 2019 | 1,64,160 |

| Sale Price of Machinery | 1,75,000 |

| Profit on the sale of the asset | 10,840 |

Note: In order to make easy calculation, the plant purchased on Jan 01, 2012, has been divided into two parts i.e.

P1 and P2. Thus,

P1: Rs 3,00,000 (sold for Rs 1,75,000 on Oct. 01, 2014)

P2: Rs 12,00,000

https://tutorstips.com/depreciation/

Comment if you have any question.

Advertisement

Also, Check out the solved question of all Chapters: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.