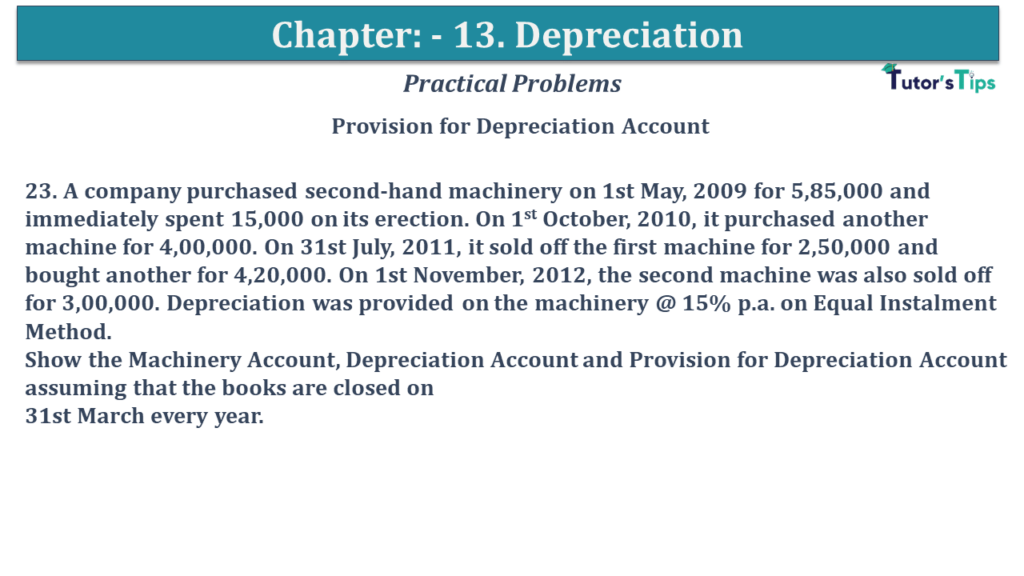

Question No 23 Chapter No 12 D K Goal

23. A company purchased second-hand machinery on 1st May, 2009 for 5,85,000 and immediately spent 15,000 on its erection. On 1st October, 2010, it purchased another machine for 4,00,000. On 31st July, 2011, it sold off the first machine for 2,50,000 and bought another for 4,20,000. On 1st November, 2012, the second machine was also sold off for 3,00,000. Depreciation was provided on the machinery @ 15% p.a. on Equal Instalment Method.

Show the Machinery Account, Depreciation Account and Provision for Depreciation Account assuming that the books are closed on 31st March every year.

The solution of Question No 23 Chapter No 12 D K Goal: –

| Dr. | Machinery A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 1stMay.2009 | To Bank A/c (5,85,000+ 15,000) | 6,00,000 | |||||

| 31st Mar 2010 | By Balance C/d | 6,00,000 | |||||

| 6,00,000 | 6,00,000 | ||||||

| 1st Apr.2010 | To Balance b/f | 6,00,000 | |||||

| 1st Oct.2010 | To Bank A/c | 4,00,000 | 31st Mar 2011 | By Balance C/d |

10,00,000 | ||

| 10,00,000 | 10,00,000 | ||||||

| 1st Apr.2011 | To Balance b/f | 10,00,000 | 1st Jul.2011 | By Provision for Depreciation A/c |

2,02,500 | ||

| 30stJul.2011 | To Bank A/c | 4,20,000 | 1st Jul.2011 | By Bank A/c (Sale) | 2,50,000 | ||

| 1st Jul.2011 | By Profit & Loss A/c | 1,47,500 | |||||

| 31st Mar 2012 | By Balance C/d(4,00,000 + 4,20,000) | 8,20,000 | |||||

| 14,20,000 | 14,20,000 | ||||||

| 1st Apr.2012 | To Balance b/f | 8,20,000 | 1st Nov.2012 | By Provision for Depreciation A/c |

1,25,000 | ||

| 1stNov.2012 | To Profit and Loss A/c | 25,000 | 1st Nov.2012 | By Bank A/c (Sale) | 3,00,000 | ||

| 31st Mar 2015 | By Balance C/d(1,60,000 + 2,00,000) | 4,20,000 |

|||||

| 8,45,000 |

8,45,000 | ||||||

| Dr. | Depreciation A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 31stMar2010 | To Provision for Depreciation A/c | 82,500 | |||||

| 31st Mar 2010 | By Profit & Loss A/c | 82,500 | |||||

| 82,500 | 82,500 | ||||||

| 31stMar.2011 | To Provision for Depreciation A/c | 1,20,000 | |||||

| 31st Mar 2011 | By Profit & Loss A/c | 1,20,000 | |||||

| 1,20,000 | 1,20,000 | ||||||

| 1st Apr.2012 | To Provision for Depreciation A/c | 1,32,000 | |||||

| 31st Mar 2012 | By Profit & Loss A/c | 1,32,000 | |||||

| 1,32,000 | 1,32,000 | ||||||

| 1st Apr.2013 | To Balance b/f | 98,000 | |||||

| 31st Mar 2013 | By Profit & Loss A/c | 98,000 | |||||

| 98,000 |

98,000 | ||||||

| Dr. | Provision for Depreciation A/c | Cr. | |||||

| Date | Particulars |

J.F. | Amount | Date | Particulars |

J.F. | Amount |

| 31st Mar 2010 | By Depreciation A/c (11 Months) | 82,500 | |||||

| 31stMar.2010 | Balance c/d | 82,500 | |||||

| 82,500 | 82,500 | ||||||

| 31st Apr 2010 | By Balance b/d | 82,500 | |||||

| 31stMar.2012 | Balance c/d | 2,02,500 | 31st Mar 2012 | By Depreciation A/c (90,000 + 30,000) | 1,20,000 | ||

| 2,02,500 | 2,02,500 | ||||||

| 31st Jul.2011 |

To Machinery A/c (82,500 + 90,000 + 30,000) |

2,02,500 | 31st Apr 2011 | By Balance b/d | 2,02,500 | ||

| 1st Jul.2011 | By Depreciation A/c (3 Months) | 30,000 | |||||

| 1st Apr.2014 | To Balance b/f | 1,32,000 | 31st Mar.2012 | By Depreciation A/c (60,000 + 42,000) | 1,02,000 | ||

| 2,03,500 | 2,03,500 | ||||||

| 1st Jan.2013 | To Machinery A/c(30,000 + 60,000 + 35,000) | 1,25,000 | 31st Apr 2012 | By Balance b/d | 1,32,000 | ||

| 31st Nov.2012 | By Depreciation A/c(7 months) | 35,000 | |||||

| 1st Apr.2013 | To Balance b/f | 1,05,000 |

31st Mar.2013 | By Depreciation A/c (24,000 + 7,500) |

63,000 | ||

| 2,30,000 | 2,30,000 | ||||||

Working Note of Question No 23 Chapter No 12 D K Goal:

Calculation of Profit or Loss on Sale Machinery 1

| Statement Showing profit or loss on the sale of Machinery | |

| Particulars |

Amount |

| Machinery Purchase on of Equipment as on 1st May. 2009 | 6,00,000 |

| Less: – Amount of Depreciation charged on the year 2009-10 | |

| 6,00,000 *15%* 6/12 | 82,000 |

| Amount of Depreciation charged on the year 2010-11 | |

| 6,00,000 *15%* 12/12 | 90,000 |

| Amount of Depreciation charged on the year 2011-12 | |

| 6,00,000 *15%* 4/12 | 30,000 |

| Book value of asset as on 30st Jul, 2011 | 3,97,500 |

| Sale Price of Machinery | 2,50,000 |

| Loss on the sale of the asset | 1,47,500 |

Calculation of Profit & Loss on Sale of Machinery 2

| Statement Showing profit or loss on the sale of Machinery | |

| Particulars |

Amount |

| Machinery Purchase on of Equipment as on 1st Oct. 2010 | 4,00,000 |

| Less: – Amount of Depreciation charged on the year 2010-11 | |

| 4,00,000 *15%* 6/12 | 30,000 |

| Amount of Depreciation charged on the year 2011-12 | |

| 4,00,000 *15%* 12/12 | 60,000 |

| Amount of Depreciation charged on the year 2012-13 | |

| 4,00,000 *15%* 7/12 | 35,000 |

| Book value of asset as of 1st Nov 2012 | 2,75,000 |

| Sale Price of Machinery | 3,00,000 |

| Profit on the sale of the asset | 25,000 |

Note: In order to make easy calculations, machinery purchased on July 01, 2015, has been divided into three parts i.e. M1, M2, and M3.

Thus,

M1: Rs 80,000 (sold for Rs 50,000 on Apr. 01, 2017)

M2: Rs 80,000 (sold for Rs 40,000 on Jan. 01, 2019)

M3: Rs 1,60,000 (includes the cost of 2 machines)

Advertisement

https://tutorstips.com/depreciation/

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST)

- Chapter 7 Books of Original Entry – Cash Book

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.