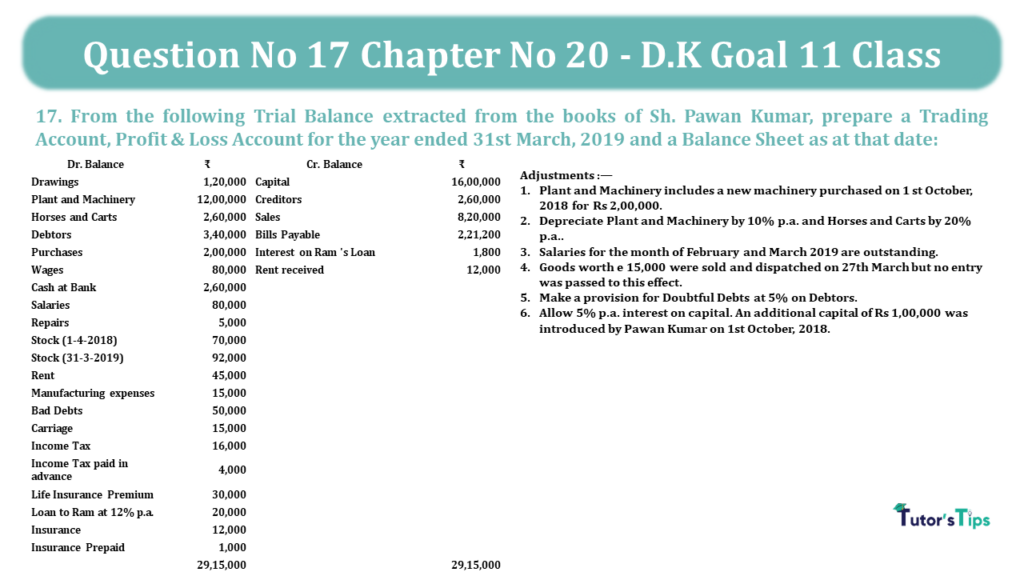

Question No 17 Chapter No 20 D.K Goal 11 Class

17. From the following Trial Balance extracted from the books of Sh. Pawan Kumar, prepare a Trading Account, Profit & Loss Account for the year ended 31st March, 2019 and a Balance Sheet as at that date:

| Dr. Balance | ₹ | Cr. Balance | ₹ |

| Drawings | 1,20,000 | Capital | 16,00,000 |

| Plant and Machinery | 12,00,000 | Creditors | 2,60,000 |

| Horses and Carts | 2,60,000 | Sales | 8,20,000 |

| Debtors | 3,40,000 | Bills Payable | 2,21,200 |

| Purchases | 2,00,000 | Interest on Ram ‘s Loan | 1,800 |

| Wages | 80,000 | Rent received | 12,000 |

| Cash at Bank | 2,60,000 | ||

| Salaries | 80,000 | ||

| Repairs | 5,000 | ||

| Stock (1-4-2018) | 70,000 | ||

| Stock (31-3-2019) | 92,000 | ||

| Rent | 45,000 | ||

| Manufacturing expenses | 15,000 | ||

| Bad Debts | 50,000 | ||

| Carriage | 15,000 | ||

| Income Tax | 16,000 | ||

| Income Tax paid in advance | 4,000 | ||

| Life Insurance Premium | 30,000 | ||

| Loan to Ram at 12% p.a. | 20,000 | ||

| Insurance | 12,000 | ||

| Insurance Prepaid | 1,000 | ||

| 29,15,000 | 29,15,000 |

Adjustments :—

1. Plant and Machinery includes a new machinery purchased on 1 st October, 2018 for Rs 2,00,000.

2. Depreciate Plant and Machinery by 10% p.a. and Horses and Carts by 20% p.a..

3. Salaries for the month of February and March 2019 are outstanding.

4. Goods worth e 15,000 were sold and dispatched on 27th March but no entry was passed to this effect.

5. Make a provision for Doubtful Debts at 5% on Debtors.

6. Allow 5% p.a. interest on capital. An additional capital of Rs 1,00,000 was introduced by Pawan Kumar on 1st October, 2018.

[Ans: G.P.₹4,55,000; N.P. ₹4,150; B/S Total ₹20,08,850.]

The Solution of Question No 17 Chapter No 20 D.K Goal 11 Class:

| Trading Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Opening stock | 70,000 | By Sale A/c | 8,20,000 | ||

| To Purchases A/c | 2,00,000 | Add:- Sale not recorded | 15,000 | 8,35,000 | |

| Add: Closing Stock(see WN1) | 92,000 | 2,92,000 | By closing stock A/c | 92,000 | |

| To Wages A/c | 80,000 | ||||

| To Carriage | 15,000 | ||||

| To Manufacturing expenses | 15,000 | ||||

| To Gross Profit A/c | 4,55,000 | ||||

| 9,27,000 | 9,27,000 | ||||

|

Profit & Loss Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Salaries A/c | 80,000 | By Gross profit b/d | 4,55,000 | ||

| Add: Outstanding Salaries(WN2) | 16,000 | 96,000 | By Interest on Ram ‘s Loan A/c | 1,800 | |

| To Repairs A/c | 5,000 | Add: Accrued Interest(WN4) | 600 | 2,400 | |

| To Rent A/c | 45,000 | By Rent Received A/c | 12,000 | ||

| To Bad Debts | 50,000 | ||||

| Add: New Prov. for D/Debts(WN3) | 17,750 | 67,750 | |||

| To Insurance A/c | 12,000 | ||||

| To Depreciation on (WN5) | |||||

| -Plant and Machinery A/c | 1,10,000 | ||||

| -Horses and Carts A/c | 52,000 | 1,62,000 | |||

| To Interest on Capital A/c (WN6) | 77,500 | ||||

| To Net Profit A/c | 4,150 | ||||

| 4,69,400 | 4,69,400 | ||||

|

Balance sheet for the year ending 31st March,2018 |

|||||

| Liabilities |

Amount | Assets |

Amount | ||

| Capital | 16,00,000 | Plant and Machinery A/c | 12,00,000 | ||

| Add: Net profit | 4,150 | Less: Depreciation | 1,10,000 | 10,90,000 | |

| Interest on Capital | 77,500 | Horses and Carts A/c | 2,60,000 | ||

| 16,04,150 | Less: Depreciation | 52,000 | 208,000 | ||

| Less: Drawing | 1,20,000 | Debtors | 3,40,000 | ||

| Income Tax | 16,000 | Add: Sale Not recorded | 15,000 | ||

| Advance Income Tax | 4,000 | Less: New provision | 17,750 | 3,37,250 | |

| Life Insurance Premium | 30,000 | 15,11,650 | Cash at Bank | 2,60,000 | |

| Creditors | 2,60,000 | Stock (31-3-2019) | 92,000 | ||

| Bills Payable | 2,21,200 | Loan to Ram at 12% p.a. | 20,000 | ||

| Outstanding Salaries A/c | 16,000 | Insurance Prepaid | 1,000 | ||

| Accrued Interest | 600 | Accrued Interest | 600 | ||

| 20,08,850 | 20,08,850 | ||||

Working Notes: –

Advertisement

WN1. Why to add closing stock in purchase?

Becasue closing stock is given in the trail balance. When closing stock is given in the trail balance then we have to add it in the purchase account.

The reason behind it that the amount of the closing stock is the part of purchase and opening stock which is left at the end of year if the closing stock is given in the trail balance it means the net amount of purchase(after deducting amount of closing stock) has given.

WN.2 Calculation of amount of Outstanding Salaries

Outstanding Salaries = Monthly Salaries X Numbers of months for salaries outstanding

Advertisement

Monthly Salaries = Salaries Paid/Number of months of Salaries Paid

= 80,000/10

= 8,000/-

Numbers of months for salaries outstanding = Feb and March i.e 2 months

So

= 8,000 X 2

= 16,000./-

Advertisement

WN.3 Calculation of New Provision for Doubtful Debts

| Amount of Debtors | 3,40,000 |

| Add: Futher Debtors | 15,000 |

| Closing Balance of Debtors | 3,55,000 |

New Provision for Doubtful Debts = Closing Balance of Debtors X Rate of Provision

= 3,55,000 X 5%

= 17,750/-

WN.4 Calculation of Accrued Interest

Advertisement

Accrued Interest = Total Amount of Interest on Loan – Interest Received

Total Amount of Interest on Loan = Loan Amount X Rate of Interest

= 20,000 X 12/100

Advertisement

= 2,400/-

Accrued Interest = 2,400 – 1,800

= 600/-

WN.5 Calculation of Depreciation on Plant and Machinery

Depreciation on opening balance= Opeing balance of Plant and Machinery X Rate of Depreciation (Full Year)

Opeing balance of Plant and Machinery = Closing balance – Purchase During year

= 12,00,000 – 2,00,000

= 10,00,000

Depreciation = 10,00,000 * 10%

= 1,00,000/-

Depreciation on purchase during the year = Plant and Machinery Purchase during the year X Rate of Depreciation (from the date of purchase to the end of year)

= 2,00,000 X 10% X 6/12

= 10,000

Total Amount of Depreciation = Depreciation on opening balance + Depreciation on purchase during the year

= 1,00,000 + 10,000

= 1,10,000/-

WN.5 Calculation of Interest on Capital

Interest on Capital on opening Capital = Opeing Capital X Rate of Interest (Full Year)

Opeing Capital = Closing Capital – Addition Capital invested during year

= 16,00,000 – 1,00,000

= 15,00,000

Interest on Capital = 15,00,000 * 5 %

= 75,000/-

Interest on Addition Capital invested during year = Addition Capital invested during year X Rate of Interest (from the date of capital invested to the end of year)

= 1,00,000 X 5% X 6/12

= 2,500

Total Amount of Interest on Capital = Interest on Capital on opening Capital + Interest on Addition Capital invested during year

= 75,000+ 2,500

= 77,500/-

Also, Check out the solved question of all Chapters: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST)

- Chapter 7 Books of Original Entry – Cash Book

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books

- Chapter 9 Ledger

- Chapter 10 Trial Balance and Errors

- Chapter 11 Bank Reconciliation Statement

- Chapter 12 Depreciation

- Chapter 13 Bills of Exchange

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts

- Chapter 20 Final Accounts – With Adjustments

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.