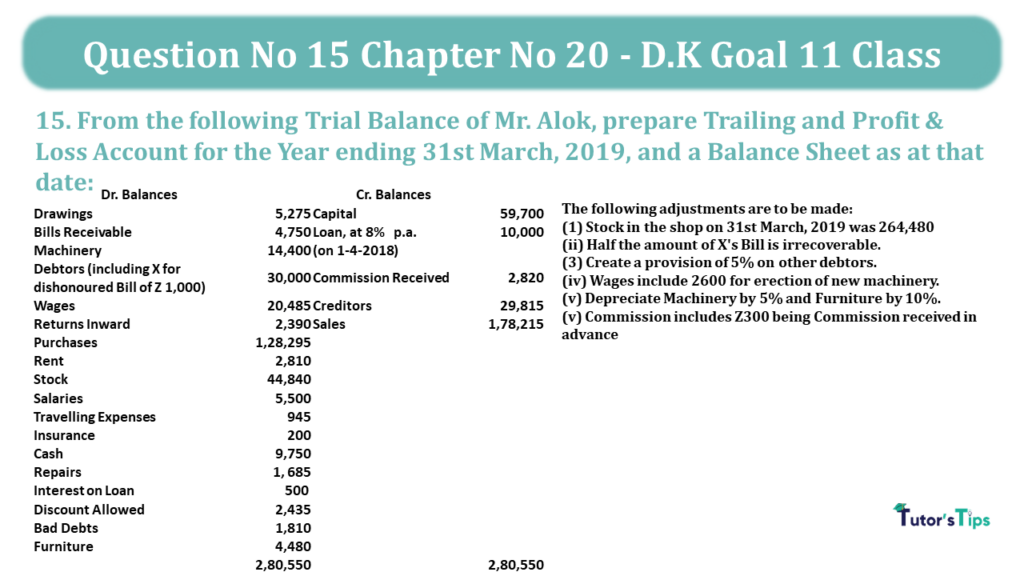

Question No 15 Chapter No 20 D.K Goal 11 Class

15. From the following Trial Balance of Mr. Alok, prepare Trailing and Profit & Loss Account for the Year ending 31st March, 2019, and a Balance Sheet as at that date:

| Dr. Balances | Cr. Balances | ||

| Drawings | 5,275 | Capital | 59,700 |

| Bills Receivable | 4,750 | Loan, at 8% p.a. (on 1-4-2018) | 10,000 |

| Machinery | 14,400 | Commission Received | 2,820 |

| Debtors (including X for dishonoured Bill of Z 1,000) | 30,000 | Creditors | 29,815 |

| Wages | 20,485 | Sales | 1,78,215 |

| Returns Inward | 2,390 | ||

| Purchases | 1,28,295 | ||

| Rent | 2,810 | ||

| Stock | 44,840 | ||

| Salaries | 5,500 | ||

| Travelling Expenses | 945 | ||

| Insurance | 200 | ||

| Cash | 9,750 | ||

| Repairs | 1, 685 | ||

| Interest on Loan | 500 | ||

| Discount Allowed | 2,435 | ||

| Bad Debts | 1,810 | ||

| Furniture | 4,480 | ||

| 2,80,550 | 2,80,550 |

The following adjustments are to be made:

(1) Stock in the shop on 31st March, 2019 was 264,480

(ii) Half the amount of X’s Bill is irrecoverable.

(3) Create a provision of 5% on other debtors.

(iv) Wages include 2600 for erection of new machinery.

(v) Depreciate Machinery by 5% and Furniture by 10%.

(v) Commission includes Z300 being Commission received in advance

[Ans. G.P. 47,285; N.P. ₹ 30,472 B/S Total 1,25,312]

The Solution of Question No 15 Chapter No 20 D.K Goal 11 Class:

| Trading Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To opening stock | 1,28,295 | By Sale A/c | 1,78,215 | ||

| To Purchases A/c | 44,840 | Less:- Returns A/c | 2,390 | 1,75,825 | |

| To wages A/c | 19,885 | By closing stock A/c | 64,480 | ||

| To Gross Profit A/c | 47,285 | ||||

| 2,40,305 | 2,40,305 | ||||

|

Profit & Loss Account |

|||||

| Particular |

Amount | Particular |

Amount | ||

| To Rent A/c | 2,810 | By Gross profit b/d | 47,285 | ||

| To salaries A/c | 5,500 | By Commission received | 2,820 | ||

| To Traveling expenses A/c | 945 | Less Received in advance | 300 | 2,520 | |

| To Insurance A/c | 200 | ||||

| To Interest on loan A/c | 500 | ||||

| Add: Outstanding | 300 | 800 | |||

| To Discount allowed A/c | 2,435 | ||||

| To Depreciation on | |||||

| -Machinery A/c | 750 | ||||

| -Furniture A/c | 448 | 1,198 | |||

| To provision for debtors | 1,450 | ||||

| To Bad debts A/c | 2,310 | ||||

| To Repairs A/c | 1,685 | ||||

| To Net Profit A/c | 30,472 | ||||

| 49,805 | 49,805 | ||||

|

Balance sheet for the year ending 31st March,2019 |

|||||

| Liabilities |

Amount | Assets |

Amount | ||

| Capital | 59,700 | Machinery A/c | 14,250 | ||

| Add: Net profit | 30,472 | Furniture A/c | 4,032 | ||

| 90,172 | Stock A/c | 64,480 | |||

| Less: Drawings A/c | 5,275 | 84,897 | Debtors A/c | 26,050 | |

| Bill receivable A/c | 4,750 | ||||

| Loan at 8% p.a A/c | 10,000 | Cash in hand | 9,750 | ||

| outstanding interest on loan A/c | 300 | ||||

| Creditors A/c | 29,815 | ||||

| Advance commission received | 300 | ||||

| 1,25,312 | 1,25,312 | ||||

Working Notes: –

Advertisement

WN.1 Calculation of book value of machinery

| Machinery value after depreciation book value of machinery | 14,400 | |

| Add: Erection value after depreciation book vale of machinery | 600 | |

| Less: Depreciation book value of machinery | 15,000 | |

| 750 | 14,250 |

WN.2 Calculation of Debtors book value

| Debtors book value | 30,000 | |

| Less: Provision for debtor | 1,450 | |

| Less: Bad debts (30,000 -1,000 discount) *5% | 500 | 28,050 |

WN.3 Calculation of Wages Debited to Profit/loss account

| Wages Debited to Profit/loss account | 20,485 | |

| Less: Wages for erection of new machinery | 600 | |

| 19,885 | ||

WN.4 Calculation of Book value of furniture

| Book value of furniture | 4480 | |

| Less: Depreciation @10% | 448 | |

| 4,032 |

Also, Check out the solved question of all Chapters: –

Advertisement

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.