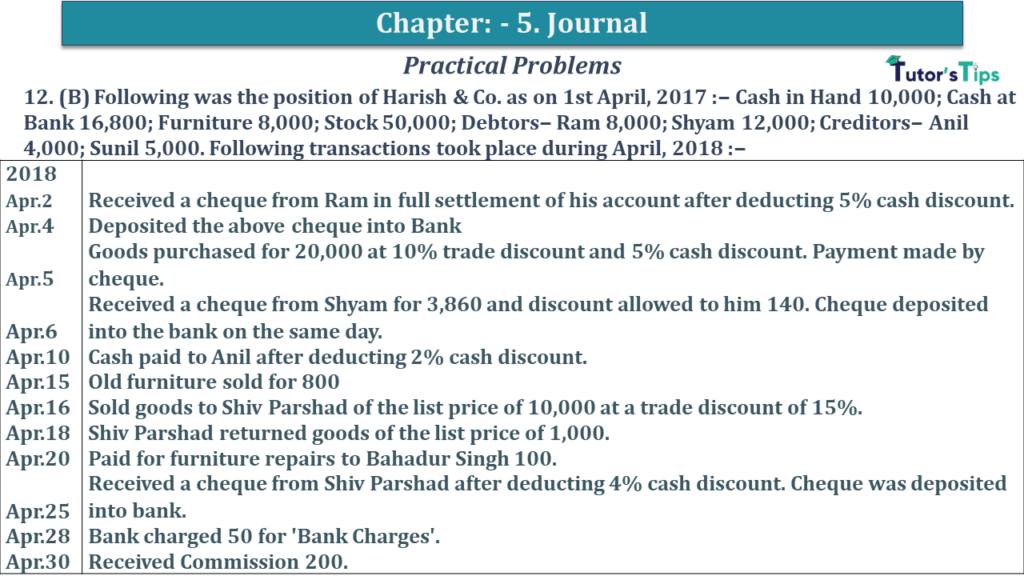

Question No 12(B) Chapter No 5

12. (B) Following was the position of Harish & Co. as on 1st April, 2017 :− Cash in Hand 10,000; Cash at Bank 16,800; Furniture 8,000; Stock 50,000; Debtors− Ram 8,000; Shyam 12,000; Creditors− Anil 4,000; Sunil 5,000. Following transactions took place during April 2018:−

| 2018 | |

| Apr.2 | Received a cheque from Ram in full settlement of his account after deducting a 5% cash discount. |

| Apr.4 | Deposited the above cheque into Bank |

| Apr.5 | Goods purchased for 20,000 at 10% trade discount and 5% cash discount. Payment made by cheque. |

| Apr.6 | Received a cheque from Shyam for 3,860 and a discount allowed to him 140. Cheque deposited into the bank on the same day. |

| Apr.10 | Cash paid to Anil after deducting 2% cash discount. |

| Apr.15 | Old furniture sold for 800 |

| Apr.16 | Sold goods to Shiv Parshad of the list price of 10,000 at a trade discount of 15%. |

| Apr.18 | Shiv Parshad returned goods of the list price of 1,000. |

| Apr.20 | Paid for furniture repairs to Bahadur Singh 100. |

| Apr.25 | Received a cheque from Shiv Parshad after deducting a 4% cash discount. A cheque was deposited into a bank. |

| Apr.28 | Bank charged 50 for ‘Bank Charges’. |

| Apr.30 | Received Commission 200. |

The solution of Question No 12(B) Chapter No 5: –

| In the Books of Hari Shankar & Co | |||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2019 | |||||

| Apr.1 | Cash in Hand A/c | Dr. | 10,000 | ||

| Cash at Bank A/c | Dr. | 16,800 | |||

| Furniture A/c | Dr. | 8,000 | |||

| Stock A/c | Dr. | 50,000 | |||

| Ram’s A/c | Dr. | 8,000 | |||

| Shyam’s A/c | Dr. | 12,000 | |||

| To Anil’s A/c | 4,000 | ||||

| To Sunil’s A/c | 5,000 | ||||

| To Capital A/c (Balancing figure) | 95,800 | ||||

| (Being balances of the previous year brought forward .) | |||||

| Apr.2 | Cheques-in-Hand A/c | Dr. | 7,600 | ||

| Discount Allowed A/c | Dr. | 400 | |||

| To Ram’s A/c | 8,000 | ||||

| (Being Cheque received from Ram in full settlement) | |||||

| Apr.4 | Bank A/c | Dr. | 7,600 | ||

| To Cheques-in-Hand A/c | 7,600 | ||||

| (Being Cheques −in −hand sent to bank) | |||||

| Apr.5 | Purchases A/c | Dr. | 18,000 | ||

| To Bank A/c | 17,100 | ||||

| To Discount Received A/c | 900 | ||||

| (Being Draft received from Mohan deposited into the bank) | |||||

| Apr.6 | Bank A/c | Dr. | 3,860 | ||

| Discount Allowed A/c | Dr. | 140 | |||

| To Shyam’s A/c | 4,000 | ||||

| (Being Cheque received from Shyam) | |||||

| Apr. 10 | Anil’s A/c | Dr. | 4,000 | ||

| To Cash A/c | 3,920 | ||||

| To Discount Received A/c | 80 | ||||

| (Being Cash paid to Anil in full settlement ) | |||||

| Apr. 15 | Cash A/c | Dr. | 800 | ||

| To Furniture A/c | 800 | ||||

| (Being Furniture sold for cash) | |||||

| Apr. 16 | Shiv Parshad’s A/c | Dr. | 8,500 | ||

| To Sales A/c | 8,500 | ||||

| (Being Goods sold to Shiv Pars had on credit) | |||||

| Apr. 18 | Sales Return A/c | Dr. | 850 | ||

| To Shiv Parshad’s A/c | 850 | ||||

| (Being goods returned by ShivParsh) | |||||

| Apr.20 | Repairs A/c | Dr. | 100 | ||

| To Cash A/c | 100 | ||||

| (Being Cash paid for the repair of furniture.) | |||||

| Apr.25 | Bank A/c | Dr. | 7,344 | ||

| Discount Allowed A/c | Dr. | 306 | |||

| To Shiv Parshad’s A/c | 7,650 | ||||

| (Being Cheque received in full settlement.) | |||||

| Apr.28 | Bank Charges A/c | Dr. | 50 | ||

| To Bank A/c | 50 | ||||

| (Being Bank charged some charges) | |||||

| Apr.28 | Bank Charges A/c | Dr. | 50 | ||

| To Bank A/c | 50 | ||||

| (Being Cash received and bad −debts written off.) | |||||

| Apr.27 | Sohan’s A/c | Dr. | 8,000 | ||

| To Bank A/c | 7,800 | ||||

| To Discount Received A/c | 200 | ||||

| (Being Cheque received from Sohan gets dishonored) | |||||

| Apr.28 | Cash A/c | Dr. | 8,400 | ||

| Bad Debts A/c | Dr. | 5,600 | |||

| To Dinesh’s A/c | 14,000 | ||||

| (Being Cash received and bad −debts written off.) | |||||

| Apr.30 | Cash A/c | Dr. | 200 | ||

| To Commission A/c | 200 | ||||

| (Being Commission received.) | |||||

Check out our article on the meaning of financial accounting:

https://tutorstips.com/introduction-to-financial-accounting/

Thanks, Please Like and share with your friends

Comment if you have any questions.

Advertisement

Also, Check out the solved question of all Chapters from the following links: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.