Question No 10 Chapter No 20

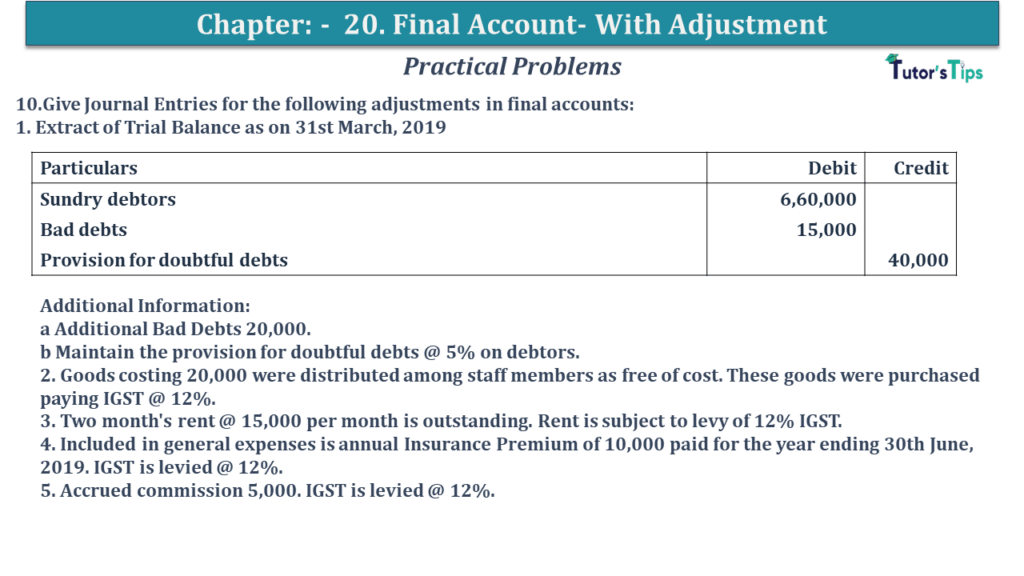

10.Give Journal Entries for the following adjustments in final accounts: 1. Extract of Trial Balance as on 31st March, 2019

| Particulars | Debit | Credit |

| Sundry debtors | 6,60,000 | |

| Bad debts | 15,000 | |

| Provision for doubtful debts | 40,000 |

Additional Information:

a Additional Bad Debts 20,000.

b Maintain the provision for doubtful debts @ 5% on debtors.

2. Goods costing 20,000 were distributed among staff members as free of cost. These goods were purchased paying IGST @ 12%.

3. Two month’s rent @ 15,000 per month is outstanding. Rent is subject to levy of 12% IGST.

4. Included in general expenses is annual Insurance Premium of 10,000 paid for the year ending 30th June, 2019. IGST is levied @ 12%.

5. Accrued commission 5,000. IGST is levied @ 12%.

The solution of Question No 10 Chapter No 20: –

| In the Books of Deepti Walia | |||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 1 | Bad debts A/c | Dr. | 20,000 | ||

| To Debtors A/c | 20,000 | ||||

| (Being further bad debts) | |||||

| Provision for Bad debts A/c | Dr. | 35,000 | |||

| To Bad Debts A/c | 35,000 | ||||

| (Being bad debts adjusted against provision ) | |||||

| Profit and Loss A/c | Dr. | 27,000 | |||

| To Provision for Bad debts A/c | 27,000 | ||||

| (Being net amount charged to P/L A/c) | |||||

| 2 | Staff welfare expenses A/c | Dr. | 22,440 | ||

| To Purchases A/c | 20,000 | ||||

| To Input IGST A/c | 2,400 | ||||

| (Being goods distributed to staff as free samples.) | |||||

| 3 | Rent A/c | Dr. | 30,000 | ||

| Input IGST A/c | Dr. | 3,600 | |||

| To outstanding rent A/c | 33,600 | ||||

| (Being outstanding rent) | |||||

| 4 | Prepaid insurance A/c | Dr. | 10,000 | ||

| To Insurance A/c | 10,000 | ||||

| (Being insurance premium paid in advance ) | |||||

| 5 | Accrued Commission A/c | Dr. | 5,600 | ||

| To Commission A/c | 5,000 | ||||

| To Output IGST A/c | 600 | ||||

| (Being commission earned but not received) | |||||

Working note:

| Calculation of bad debts to be transferred to Statement of Profit and Loss: |

||

| Particular |

Amount | |

| Bad debts | 15,000 | |

| Add: further bad debts | 20,000 | |

| Add: New provision of bad debts | 32,000 | |

| Less: Old provision of bad debts | 40,000 | |

| Bad debts transferred to Statement of Profit and Loss | 27,000 | |

| Where | ||

| New provision = 6, 60, 000– 20, 000 × 5% | 32,000 | |

https://tutorstips.com/trading-account/

Also, Check out the solved question of all Chapters: –

Advertisement

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.