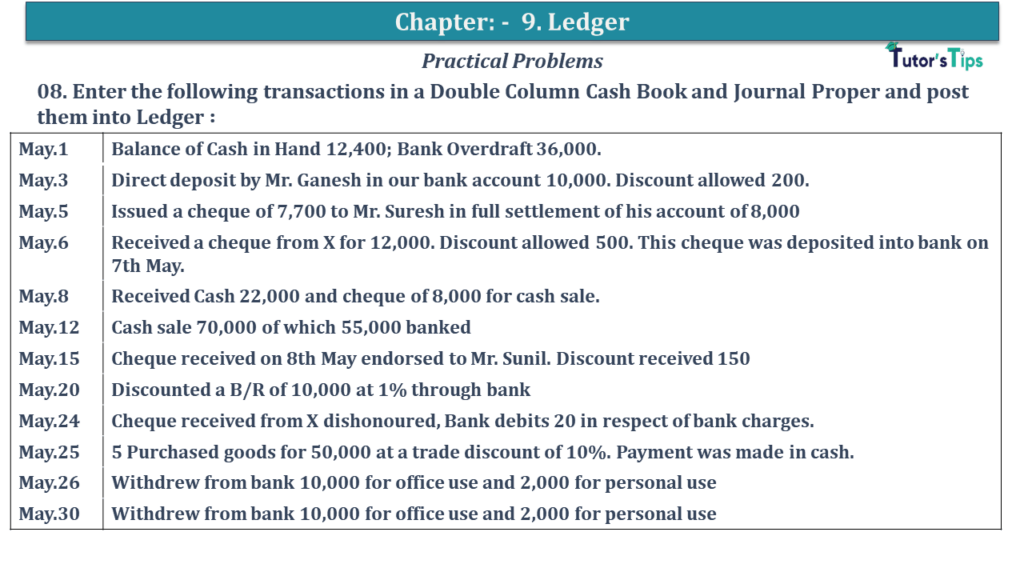

Question No 08 Chapter No 9

01. Journalise the following transaction, post them into Ledger, Balance the accounts and prepare a Trial Balance.

| May.1 |

Balance of Cash in Hand 12,400; Bank Overdraft 36,000. |

| May.3 |

Direct deposit by Mr. Ganesh in our bank account 10,000. Discount allowed 200. |

| May.5 |

Issued a cheque of 7,700 to Mr. Suresh in full settlement of his account of 8,000 |

| May.6 |

Received a cheque from X for 12,000. Discount allowed 500. This cheque was deposited into bank on 7th May. |

| May.8 |

Received Cash 22,000 and cheque of 8,000 for cash sale. |

| May.12 |

Cash sale 70,000 of which 55,000 banked |

| May.15 |

The cheque received on 8th May endorsed to Mr. Sunil. Discount received 150 |

| May.20 |

Discounted a B/R of 10,000 at 1% through bank |

| May.24 |

Cheque received from X dishonored, Bank debits 20 in respect of bank charges. |

| May.25 |

5 Purchased goods for 50,000 at a trade discount of 10%. The payment was made in cash. |

| May.26 |

Withdrew from bank 10,000 for office use and 2,000 for personal use |

| May.30 |

Withdrew from bank 10,000 for office use and 2,000 for personal use |

The solution of Question No 08 Chapter No 9: –

| Dr. |

Cash Book |

Cr. |

| Date |

Particulars

|

L.

F. |

Discount

Allowed |

Cash |

Bank |

Date |

Particulars

|

L.

F. |

Discount Received |

Cash |

Bank |

| 2020 |

|

|

|

|

|

2020 |

|

|

|

|

|

| May.1 |

To Balance c/d |

|

– |

12,400 |

– |

May.1 |

By Balance b/d |

|

– |

– |

36,000 |

| May.03 |

To Ganesh’s A/c |

|

200 |

– |

10,000 |

May.5 |

By Suresh’s A/c |

|

– |

– |

7,700 |

| May.07 |

To X A/c |

|

500 |

– |

12,000 |

May.24 |

By X A/c |

|

– |

– |

12,000 |

| May.08 |

To Sales A/c |

|

– |

22,000 |

– |

May.24 |

By Bank Charges A/c |

|

– |

– |

20 |

| May.12 |

To Sales A/c |

|

– |

15,000 |

55,000 |

May.25 |

By Purchase A/c |

|

|

45,000 |

– |

| May.20 |

To Bills Receivable A A/c |

|

– |

– |

9,900 |

May.26 |

By Cash A/c |

|

– |

– |

10,000 |

| May.26 |

To Bank A/c |

|

|

10,000 |

|

May.26 |

By Drawings A/c |

|

|

|

2,000 |

| |

|

|

|

|

|

May.31 |

By Interest A/c |

|

|

|

4,500 |

| |

|

|

|

|

|

|

|

|

|

|

|

| May.31 |

To Balance c/d |

|

700 |

– |

– |

May.31 |

By Balance C/d |

|

–

|

14,400 |

14,680 |

| |

|

|

700 |

59,400 |

86,900 |

|

|

|

– |

59,400 |

86,900 |

In the Books of Radhika Traders

|

| Date |

Particulars

|

L.F. |

Debit |

Credit |

| 2019 |

|

|

|

|

|

| May 06 |

Cheques-in-Hand A/c |

Dr. |

|

12,000 |

|

| |

Discount Allowed A/c |

Dr. |

|

500 |

|

| |

To X A/c |

|

|

|

12,500 |

| |

(Being Cheque received from X but not banked) |

|

|

|

| |

|

|

|

|

|

| May.8 |

Cheques-in-Hand A/c |

Dr. |

|

8,000 |

|

| |

To Cash A/c |

|

|

8,000 |

| |

(Being Cheque received for sales but not banked) |

|

|

|

| |

|

|

|

|

| May 15 |

Sunil’s A/c |

Dr. |

|

8,150 |

|

| |

To Cheques-in-Hand A/c |

|

|

|

8,000 |

| |

To Discount Received A/c |

|

|

|

150 |

| |

(Being Cheque received from sales endorsed to Sunil ) |

|

|

|

|

| |

|

|

|

|

|

| May.20 |

Discounting Charges A/c |

Dr. |

|

100 |

|

| |

To Bills Receivable A/c |

|

|

|

100 |

| |

(Being Bills receivable discounted with bank ) |

|

|

|

|

| |

|

|

|

|

|

| May.24 |

X A/c |

Dr. |

|

500 |

|

| |

To Discount Allowed A/c |

|

|

|

500 |

| |

(Being Discount canceled) |

|

|

|

|

| |

|

|

|

|

| Dr. |

Discount Allowed A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.03 |

By Ganesh’s A/c |

|

500 |

May.24 |

By X A/c |

|

500 |

| May.06 |

By X A/c |

|

200 |

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

200 |

| |

|

|

700 |

|

|

|

700 |

| Dr. |

Discount Received A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

May.05 |

By Suresh’s A/c |

|

300 |

| |

|

|

|

May.15 |

By Sunil’s A/c |

|

150 |

| May. 31 |

To Balance c/d |

|

450 |

|

|

|

|

| |

|

|

450 |

|

|

|

450 |

| Dr. |

Cheques-in-Hand Account A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.06 |

To X’s A/c |

|

12,000 |

May.07 |

To Bank A/c |

|

12,000 |

| May.08 |

To Sales A/c |

|

8,000 |

May.15 |

To Sunil’s A/c |

|

8,000 |

| |

|

|

20,000 |

|

|

|

20,000 |

| Dr. |

Discounting Charges A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.20 |

To Bills Receivable A/c |

|

100 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

100 |

| |

|

|

100 |

|

|

|

100 |

| Dr. |

Bills Receivable A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

May.1 |

By Bank A/c |

|

9,900 |

| |

|

|

|

May.1 |

By Discounting Charges A/c |

|

100 |

| May.31 |

To Balance c/d |

|

10,000 |

|

|

|

|

| |

|

|

10,000 |

|

|

|

10,000 |

| Dr. |

Ganesh’s A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

May.1 |

By Bank A/c |

|

10,000 |

| |

|

|

|

May.1 |

By Discounting Charges A/c |

|

200 |

| |

|

|

|

|

|

|

|

| May.31 |

To Balance c/d |

|

10,200 |

|

|

|

|

| |

|

|

10,200 |

|

|

|

10,200 |

| Dr. |

Purchases Return A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

Mar.6 |

By Raghu’s A/c |

|

4,000 |

| |

|

|

|

|

|

|

|

| Mar.31 |

To Balance c/d |

|

4,000 |

|

|

|

|

| |

|

|

4,000 |

|

|

|

4,000 |

| Dr. |

X’s A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.24 |

To Bank A/c |

|

12,000 |

May.06 |

By Cheques-in-Hand A/c |

|

12,000 |

| May.24 |

To Discount Allowed A/c |

|

500 |

May.06 |

By Discount Allowed A/c |

|

500 |

| |

|

|

|

|

|

|

|

| |

|

|

12,500 |

|

|

|

12,500 |

| Dr. |

Sales A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

May.08 |

By Cash A/c |

|

22,000 |

| |

|

|

|

May.08 |

By Cheques-in-Hand A/c |

|

8,000 |

| |

|

|

|

May.15 |

By Cash A/c |

|

15,000 |

| |

|

|

|

May.15 |

By Bank A/c |

|

55,000 |

| May.31 |

To Balance c/d |

|

1,00,000 |

|

|

|

|

| |

|

|

1,00,000 |

|

|

|

1,00,000 |

| Dr. |

Suresh’s A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.05 |

To Bank A/c |

|

7,700 |

|

|

|

|

| May.05 |

To Discount Received A/c |

|

300 |

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

8,000 |

| |

|

|

8,000 |

|

|

|

8,000 |

| Dr. |

Bank Charges A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.24 |

To Bank A/c |

|

20 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

20 |

| |

|

|

20 |

|

|

|

20 |

| Dr. |

Purchases A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.25 |

To Bank A/c |

|

45,000 |

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

45,000 |

| |

|

|

45,000 |

|

|

|

45,000 |

| Dr. |

Drawings A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.26 |

To Bank A/c |

|

2,000 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

2,000 |

| |

|

|

2,000 |

|

|

|

2,000 |

| Dr. |

Interest A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.31 |

To Bank A/c |

|

4,500 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

4,500 |

| |

|

|

4,500 |

|

|

|

4,500 |

| Dr. |

Sunil’s A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| May.15 |

To Cheques-in-Hand A/c |

|

8,000 |

|

|

|

|

| May.15 |

To Discount Received A/c |

|

150 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

May. 31 |

By Balance c/d |

|

8,150 |

| |

|

|

8,150 |

|

|

|

8,150 |

https://tutorstips.com/ledger/

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.

D K Goel accountancy +1 – ISC_Accounts_11_20_Image

D K Goel accountancy +1 – ISC_Accounts_11_20_Image