Question No 08 Chapter No 11

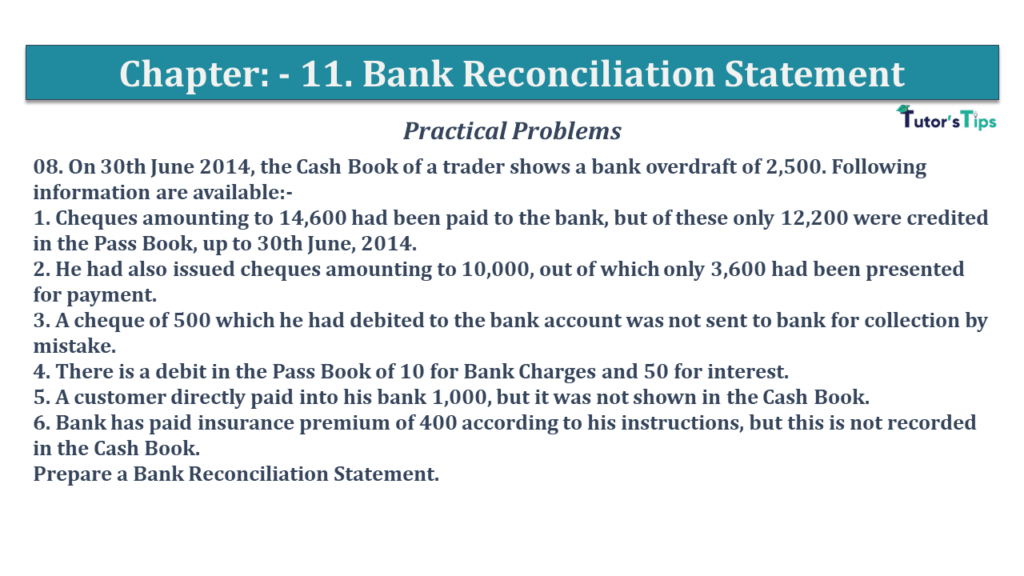

08. On 30th June 2014, the Cash Book of a trader shows a bank overdraft of 2,500. The following information is available:-

1. Cheques amounting to 14,600 had been paid to the bank, but of these only 12,200 were credited in the Pass Book, up to 30th June 2014.

2. He had also issued cheques amounting to 10,000, out of which only 3,600 had been presented for payment.

3. A cheque of 500 which he had debited to the bank account was not sent to the bank for collection by mistake.

4. There is a debit in the Pass Book of 10 for Bank Charges and 50 for interest.

5. A customer directly paid into his bank 1,000, but it was not shown in the Cash Book.

6. Bank has paid an insurance premium of 400 according to his instructions, but this is not recorded in the Cash Book.

Prepare a Bank Reconciliation Statement.

The solution of Question No 08 Chapter No 11: –

| Bank Reconciliation Statement |

||

| Particular | Plus Items (Rs) |

Minus Items (Rs) |

| Credit Balance (Overdraft) as per Cash Book | 2,500 | |

| Add 2. Cheques issued but not presented (10,000 – 3,600) | 6,400 | |

| 5. Amount directly deposited by the customer | 1,000 | |

| Less: 1. Cheque paid into bank but not credited (14,600 – 12,200) | 2,400 | |

| 4. Bank charges | 10 | |

| 4. Bank interest | 50 | |

| 3. Cheque not sent to bank for collection | 500 | |

| 6. Insurance premium paid by bank as per standing instructions | 400 | |

| Credit Balance as per Pass Book | 1,540 | |

| 7,400 | 7,400 | |

https://tutorstips.com/bank-reconciliation-statement/

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Advertisement

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.