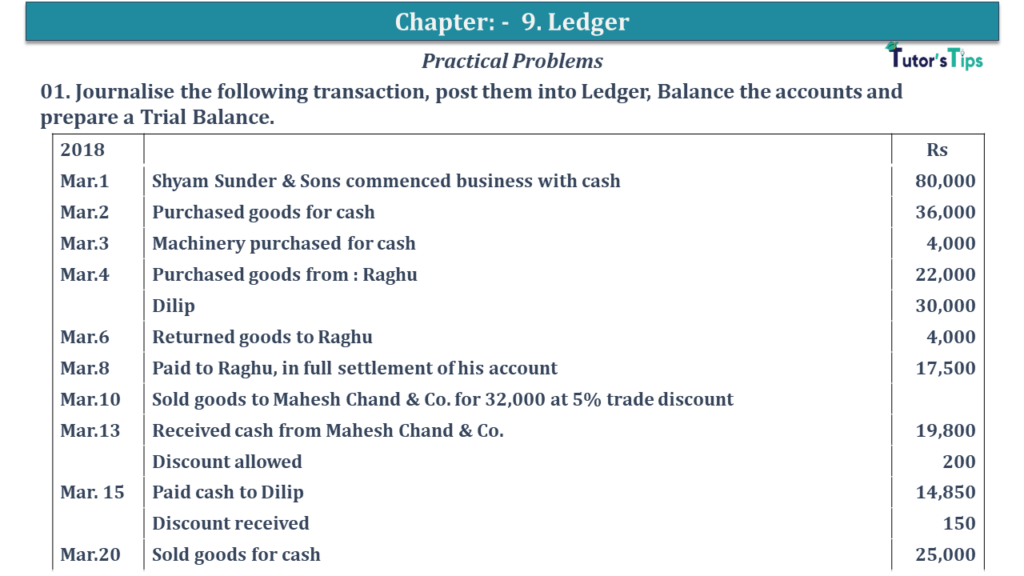

Question No 01 Chapter No 9

01. Journalise the following transaction, post them into Ledger, Balance the accounts and prepare a Trial Balance.

| 2018 |

|

Rs |

| Mar.1 |

Shyam Sunder & Sons commenced business with cash |

80,000 |

| Mar.2 |

Purchased goods for cash |

36,000 |

| Mar.3 |

Machinery purchased for cash |

4,000 |

| Mar.4 |

Purchased goods from : Raghu |

22,000 |

| |

Dilip |

30,000 |

| Mar.6 |

Returned goods to Raghu |

4,000 |

| Mar.8 |

Paid to Raghu, in full settlement of his account |

17,500 |

| Mar.10 |

Sold goods to Mahesh Chand & Co. for 32,000 at 5% trade discount |

|

| Mar.13 |

Received cash from Mahesh Chand & Co. |

19,800 |

| |

Discount allowed |

200 |

| Mar. 15 |

Paid cash to Dilip |

14,850 |

| |

Discount received |

150 |

| Mar.20 |

Sold goods for cash |

25,000 |

| Mar.24 |

Sold goods for cash to Sudhir Ltd |

18,000 |

| Mar.15 |

Paid for Rent |

1,500 |

| Mar.16 |

Received for Commission |

2,000 |

| Mar.28 |

Withdrew by Proprietor for his personal use |

5,000 |

| Mar.28 |

Purchased a fan for Proprietor’s house |

1,200 |

The solution of Question No 01 Chapter No 9: –

In the Books of Radhika Traders

|

| Date |

Particulars

|

L.F. |

Debit |

Credit |

| 2019 |

|

|

|

|

|

| Mar.1 |

Cash A/c |

Dr. |

|

80,000 |

|

| |

To Capital A/c |

|

|

|

80,000 |

| |

(Being business started with cash) |

|

|

|

| |

|

|

|

|

|

| Mar.2 |

Purchases A/c |

Dr. |

|

36,000 |

|

| |

To Cash A/c |

|

|

36,000 |

| |

(Being Goods purchased for cash) |

|

|

|

| |

|

|

|

|

| Mar.3 |

Machinery A/c |

Dr. |

|

80,000 |

|

| |

To Cash A/c |

|

|

|

80,000 |

| |

(Being Machinery purchased for cash) |

|

|

|

|

| |

|

|

|

|

|

| Mar.4 |

Purchases A/c |

Dr. |

|

52,000 |

|

| |

To Raghu’s A/c |

|

|

|

22,000 |

| |

To Dilip’s A/c |

|

|

|

30,000 |

| |

(Being Goods purchased on credit from Raghu and Dilip) |

|

|

|

|

| |

|

|

|

|

|

| Mar.6 |

Raghu’s A/c |

Dr. |

|

4,000 |

|

| |

To Purchases Return A/c |

|

|

|

4,000 |

| |

(Being Goods returned to Raghu) |

|

|

|

|

| |

|

|

|

|

|

| Mar.8 |

Raghu’s A/c |

Dr. |

|

18,000 |

|

| |

To Cash A/c |

|

|

|

17,500 |

| |

To Discount Received A/c |

|

|

|

500 |

| |

(Being Cash paid to Raghu in full settlement) |

|

|

|

|

| |

|

|

|

|

|

| Mar.10 |

Mahesh Chand & Co |

Dr. |

|

30,400 |

|

| |

To Sale A/c |

|

|

|

30,400 |

| |

(Being Goods sold to Mahesh Chand & Co. at trade discount) |

|

|

|

|

| |

|

|

|

|

|

| Mar.13 |

Cash A/c |

Dr. |

|

19,800 |

|

| |

Discount Allowed A/c |

Dr. |

|

200 |

|

| |

To Mahesh Chand & Co. |

|

|

|

20,000 |

| |

(Being Cash received from Mahesh Chand & Co.) |

|

|

|

|

| |

|

|

|

|

|

| Mar.15 |

Dilip’s A/c |

Dr. |

|

15,000 |

|

| |

To Cash A/c |

|

|

|

14,850 |

| |

To Discount Received A/c |

|

|

|

150 |

| |

(Being Cash paid to Dilip) |

|

|

|

|

| |

|

|

|

|

|

| Mar.20 |

Cash A/c |

Dr. |

|

25,000 |

|

| |

To Sales A/c |

|

|

|

25,000 |

| |

(Being Goods sold for cash) |

|

|

|

|

| |

|

|

|

|

|

| Mar.24 |

Cash A/c |

Dr. |

|

18,000 |

|

| |

To Sale A/c |

|

|

|

18,000 |

| |

(Being Goods sold for cash) |

|

|

|

|

| |

|

|

|

|

|

| Mar.25 |

Rent A/c |

Dr. |

|

1,500 |

|

| |

To Cash A/c |

|

|

|

1,500 |

| |

(Being Rent paid.) |

|

|

|

|

| |

|

|

|

|

|

| Mar.26 |

Cash A/c |

Dr. |

|

2,000 |

|

| |

To Commission A/c |

|

|

|

2,000 |

| |

(Being Commission received) |

|

|

|

|

| |

|

|

|

|

|

| Mar.28 |

Drawings A/c |

Dr. |

|

6,200 |

|

| |

To Cash A/c |

|

|

|

6,200 |

| |

(Being Cash withdrawn and fan purchased for personal use) |

|

|

|

|

| |

|

|

|

|

| Dr. |

Cash A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar. 1 |

To Capital A/c |

|

80,000 |

Mar. 2 |

By Purchases A/c |

|

36,000 |

| Mar.13 |

To Mahesh Chand & Co. A/c |

|

19,800 |

Mar.3 |

By Machinery A/c |

|

4,000 |

| Mar.20 |

To Sales A/c |

|

25,000 |

Mar.8 |

By Raghu’s A/c |

|

17,500 |

| Mar.24 |

To Sales A/c |

|

18,000 |

Mar.15 |

To Dilip’s A/c |

|

14,850 |

| Mar.26 |

To Commission A/c |

|

2,000 |

Mar.25 |

To Rent A/c |

|

1,500 |

| |

|

|

|

Mar.28 |

By Drawings A/c |

|

6,200 |

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

64,750 |

| |

|

|

1,44,800 |

|

|

|

1,44,800 |

| Dr. |

Capital A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

Mar. 1 |

By Cash A/c |

|

80,000 |

| Mar. 31 |

To Balance c/d |

|

80,000 |

|

|

|

|

| |

|

|

80,000 |

|

|

|

80,000 |

| Dr. |

Purchases A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar. 1 |

To Cash A/c |

|

36,000 |

|

|

|

|

| Mar.13 |

To Raghu’s A/c |

|

22,000 |

|

|

|

|

| Mar.20 |

To Dilip’s A/c |

|

30,000 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

88,000 |

| |

|

|

88,000 |

|

|

|

88,000 |

| Dr. |

Machinery A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.3 |

To Cash A/c |

|

4,000 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

4,000 |

| |

|

|

4,000 |

|

|

|

4,000 |

| Dr. |

Raghu’s A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.6 |

To Purchases Return A/c |

|

4,000 |

Mar.4 |

By Purchases A/c |

|

22,000 |

| Mar.8 |

To Cash A/c |

|

17,500 |

|

|

|

|

| Mar.8 |

To Discount Received A/c |

|

500 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

22,000 |

|

|

|

22,000 |

| Dr. |

Dilip’s A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.15 |

To Purchases Return A/c |

|

14,850 |

Mar.4 |

By Purchases A/c |

|

30,000 |

| Mar.15 |

To Cash A/c |

|

150 |

|

|

|

|

| |

|

|

|

|

|

|

|

| Mar.31 |

To Balance c/d |

|

15,000 |

|

|

|

|

| |

|

|

30,000 |

|

|

|

30,000 |

| Dr. |

Purchases Return A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

Mar.6 |

By Raghu’s A/c |

|

4,000 |

| |

|

|

|

|

|

|

|

| Mar.31 |

To Balance c/d |

|

4,000 |

|

|

|

|

| |

|

|

4,000 |

|

|

|

4,000 |

| Dr. |

Discount Allowed A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.13 |

To Mahesh Chand & Co A/c |

|

200 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

200 |

| |

|

|

200 |

|

|

|

200 |

| Dr. |

Discount Received A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

Mar.8 |

By Raghu’s A/c |

|

500 |

| |

|

|

|

Mar.15 |

By Dilip’s A/c |

|

150 |

| Mar.31 |

To Balance c/d |

|

650 |

|

|

|

|

| |

|

|

650 |

|

|

|

650 |

| Dr. |

Mahesh Chand & Co A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.10 |

To Sales A/c |

|

30,400 |

Mar.13 |

By Cash A/c |

|

19,800 |

| |

|

|

|

Mar.13 |

By Discount

Allowed A/c |

|

200 |

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

10,400 |

| |

|

|

30,400 |

|

|

|

30,400 |

| Dr. |

Rent A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.25 |

To Cash A/c |

|

1,500 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

1,500 |

| |

|

|

1,500 |

|

|

|

1,500 |

| Dr. |

Commission A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

Mar.26 |

By Cash A/c |

|

2,000 |

| Mar.31 |

To Balance c/d |

|

2,000 |

|

|

|

|

| |

|

|

2,000 |

|

|

|

2,000 |

| Dr. |

DrawingsA/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| Mar.28 |

To Cash A/c |

|

6,200 |

|

|

|

|

| |

|

|

|

|

|

|

|

| |

|

|

|

Mar. 31 |

By Balance c/d |

|

6,200 |

| |

|

|

6,200 |

|

|

|

6,200 |

| Dr. |

Sales A/c |

Cr. |

| Date |

Particulars

|

J.F. |

Amount |

Date |

Particulars

|

J.F. |

Amount |

| 2018 |

|

|

|

2018 |

|

|

|

| |

|

|

|

Mar.10 |

By Mahesh Chand & Co A/c |

|

30,400 |

| |

|

|

|

Mar.20 |

By Cash A/c |

|

25,000 |

| |

|

|

|

Mar.24 |

By Cash A/c |

|

18,000 |

| Mar.31 |

To Balance c/d |

|

73,400 |

|

|

|

|

| |

|

|

73,400 |

|

|

|

73,400 |

| Trail Balance A/c |

Particulars

|

J.F. |

Debit |

Credit |

| Cash A/c |

|

64,750 |

|

| Capital A/c |

|

|

80,000 |

| Purchases A/c |

|

88,000 |

|

| Machinery A/c |

|

4,000 |

|

| Dilip’s A/c |

|

|

15,000 |

| Purchases Return A/c |

|

|

4,000 |

| Discount Received A/c |

|

|

650 |

| Discount Allowed A/c |

|

200 |

|

| Mahesh Chand & Co. A/c |

|

10,400 |

|

| Rent A/c |

|

1,500 |

|

| Commission A/c |

|

|

2,000 |

| Drawings A/c |

|

6,200 |

|

| Sales A/c |

|

|

73,400 |

| |

|

1,75,050 |

1,75,050 |

https://tutorstips.com/ledger/

Thanks, Please Like and share with your friends

Comment if you have any question.

Also, Check out the solved question of all Chapters: –

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.

D K Goel accountancy +1 – ISC_Accounts_11_20_Image

D K Goel accountancy +1 – ISC_Accounts_11_20_Image