Question No 20 Chapter No 13

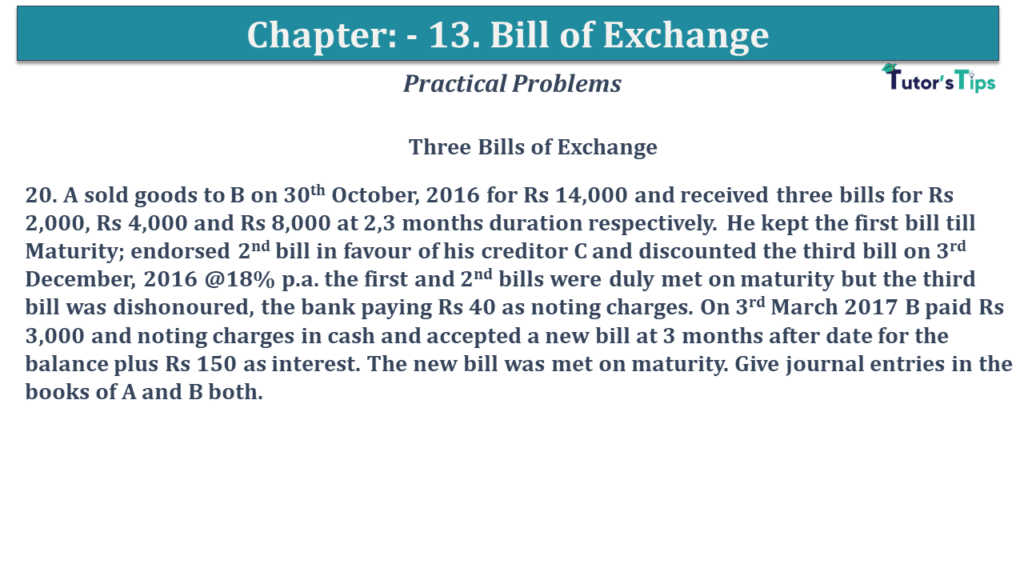

Three Bills of Exchange

20. A sold goods to B on 30th October, 2016 for Rs 14,000 and received three bills for Rs 2,000, Rs 4,000 and Rs 8,000 at 2,3 months duration respectively. He kept the first bill till Maturity; endorsed 2nd bill in favour of his creditor C and discounted the third bill on 3rd December, 2016 @18% p.a. the first and 2nd bills were duly met on maturity but the third bill was dishonoured, the bank paying Rs 40 as noting charges. On 3rd March 2017 B paid Rs 3,000 and noting charges in cash and accepted a new bill at 3 months after date for the balance plus Rs 150 as interest. The new bill was met on maturity. Give journal entries in the books of A and B both.

The solution of Question No 20 Chapter No 13: –

| In the books of A |

|||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2018 | |||||

| Oct.30 | B A/c | Dr. | 14,000 | ||

| To Sale A/c | 14,000 | ||||

| (Being Sold goods to B) | |||||

| Oct.30 | Bill Receivable A/c (i) | Dr. | 2,000 | ||

| Bill Receivable A/c (ii) | Dr. | 4,000 | |||

| Bill Receivable A/c (iii) | Dr. | 8,000 | |||

| To B A/c | 14,000 | ||||

| (Being three bills drew on B and acceptance received from him.) | |||||

| Oct.30 | C A/c | Dr. | 4,000 | ||

| To Bill Receivable A/c (ii) | 4,000 | ||||

| (Being bill endorsed to C ) | |||||

| Dec.3 | Bank A/c | Dr. | 7,760 | ||

| Discount A/c | Dr. | 240 | |||

| To Bill Receivable A/c | 8,000 | ||||

| (Being third bill was discounted by A) | |||||

| Jan.2 | Cash A/c | Dr. | 2,000 | ||

| To Bill Receivable A/c (i) | 2,000 | ||||

| (Being bill received on maturity) | |||||

| Feb.3 | Bill Receivable A/c | Dr. | 8,000 | ||

| Noting Charges A/c | Dr. | 40 | |||

| To noting Charges A/c | 8,040 | ||||

| (Being third bill was dishonoured ) | |||||

| Feb.3 | Cash A/c | Dr. | 3,040 | ||

| To Noting Charges A/c | 3,000 | ||||

| To B A/c | 40 | ||||

| (Being third bill was dishonoured ) | |||||

| Feb.3 | B A/c | Dr. | 150 | ||

| To Interest A/c | 150 | ||||

| (Being charged interest on B) | |||||

| Feb.3 | Bill Receivable A/c (iv) | Dr. | 5,150 | ||

| To B A/c | 5,150 | ||||

| (Being new bill drawn on harish ) | |||||

| Apr.7 | Cash A/c | Dr. | 5,150 | ||

| To Bill Receivable A/c (iv) | 5,150 | ||||

| (Being bill was mat on maturity) | |||||

| In the books of B |

|||||

| Date | Particulars |

L.F. | Debit | Credit | |

| 2018 | |||||

| Oct.30 | Purchases A/c | Dr. | 14,000 | ||

| To A A/c | 14,000 | ||||

| (Being purchases goods from A) | |||||

| Oct.30 | A A/c | Dr. | 14,000 | ||

| To Bill Payable A/c (i) | 2,000 | ||||

| To Bill Payable A/c (ii) | 4,000 | ||||

| To Bill Payable A/c (iii) | 8,000 | ||||

| (Being three bills drew by Satish acceptance by us.) | |||||

| Jan.2 | Bill Payable A/c (i) | Dr. | 2,000 | ||

| To Cash A/c | 2,000 | ||||

| (Being first bill payable paid on maturity) | |||||

| Feb.02 | Bill Payable A/c(ii) | Dr. | 4,000 | ||

| To Satish A/c | 4,000 | ||||

| (Being Bill dishonoured) | |||||

| Mar.04 | Bill Payable A/c (iii) | Dr. | 8,000 | ||

| A A/c | 8,000 | ||||

| (Being third bill was dishonoured ) | |||||

| Mar.04 | A A/c (iii) | Dr. | 3,000 | ||

| Noting Charges A/c | Dr. | 40 | |||

| To Cash A/c | 3,040 | ||||

| (Being Cash paid and noting charges paid to A) | |||||

| Mar.04 | A A/c | Dr. | 5,150 | ||

| To Bill Payable A/c (iii) | 5,150 | ||||

| (Being bill paid on maturity) | |||||

| Mar.04 | Bill Payable A/c (iv) | Dr. | 5,150 | ||

| To Cash A/c | 5,150 | ||||

| (The being bill was a mat on maturity) | |||||

Working Note: –

Calculation of Discounting Charges

| Discounting Charges | = | 8,000 | x | 18 | X | 2 |

| 100 | 12 | |||||

| = | Rs 240 |

https://tutorstips.com/bills-payable/

Advertisement

Also, Check out the solved question of all Chapters: –

D K Goel – New ISC Accountancy -(Class 11 – ICSE)- Solution

- Chapter 1 Evolution of Accounting & Basic Accounting Terms

- Chapter 2 Accounting Equations

- Chapter 3 Meaning and Objectives of Accounting

- Chapter 4 Double Entry System

- Chapter 5 Books of Original Entry – Journal

- Chapter 6 Accounting for Goods and Service Tax (GST) (Coming soon)

- Chapter 7 Books of Original Entry – Cash Book (Coming soon)

- Chapter 8 Books of Original Entry – Special Purpose Subsidiary Books (Coming soon)

- Chapter 9 Ledger (Coming soon)

- Chapter 10 Trial Balance and Errors (Coming soon)

- Chapter 11 Bank Reconciliation Statement (Coming soon)

- Chapter 12 Depreciation (Coming soon)

- Chapter 13 Bills of Exchange (Coming soon)

- Chapter 14 Generally Accepted Accounting Principles(GAAP)

- Chapter 15 Bases of Accounting

- Chapter 16 Accounting Standards and International Financial Reporting Standard(IFRS) (Coming soon)

- Chapter 17 Capital and Revenue

- Chapter 18 Provisions and Reserves

- Chapter 19 Final Accounts (Coming soon)

- Chapter 20 Final Accounts – With Adjustments (Coming soon)

- Chapter 21 Errors and their Rectification (Coming soon)

- Chapter 22 Accounts from Incomplete Records – Single Entry System (Coming soon)

- Chapter 23 Accounts of Not-for-Profit Organisations (Coming soon)

- Chapter 24 Computerised Accounting System (Coming soon)

- Chapter 25 Introduction to Accounting Information System (Coming soon)

Check out the Accountancy Class +1 by D.K. Goal (Arya Publication) from their official Site.